Insurance distribution pt. 4 - Which horse to pick

Bottoms-up & top-down analysis of insurance brokers

In part 1 we gave an introduction to the insurance distribution ecosystem, and in parts 2 & 3 we walked through the causes of the recent major repricing of brokers down to 15-17 NTM earnings.

In parts 2 & 3, we laid out a framework that mapped AI risk & cycle risk to different parameters - wholesale vs retail, large vs small clients, etc.

If we were management consultants, that mapping would lead to a nice 4x4 quadrant (AI risk on x-axis, market cycle risk on Y-axis) that could give the reader a neat and perfect answer to where to invest based on their view of the future. By the grace of God and his eternal mercy, we have fortunately been spared the management consultant fate.

The truth is that each business is unique. Some of them have amazing management teams and ludicrous track records within M&A, while others have more blemished records. Some are facing major integrations of large acquisitions, while others are struggling with their organic business.

We are firm believers that all stock-picking should be done bottoms-up. You buy into a company as a partial owner - you don’t buy “an exposure” to a set of factors. You can consider secular trends, but you have to start with a strong operational foundation and hopefully deep moats.

With that said, some of the brokers are more well-suited for people with a view of AI, and others with a view of the cycle. So let’s take the top-down assessment up-front, and briefly, before we dive into the meat & potatoes of which company has the fundamentals in order.

The top-down assessment

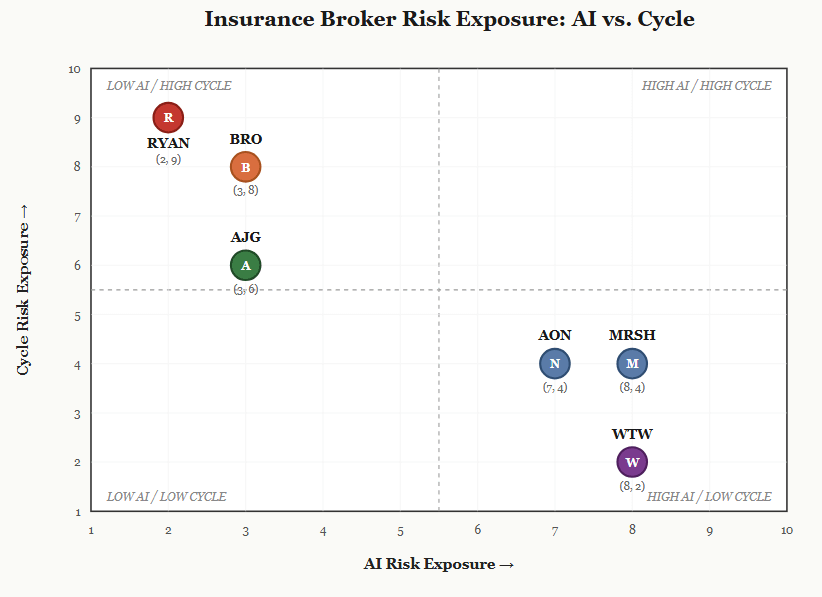

Channelling our inner management consultants, the below is a 4-by-4 diagram of AI risk and market cycle risk. It goes 1-10 for each, 10 being the highest, and illustrates which of the macro risks are dominant for each. Claude was helpful in visualizing:

Ryan - High cycle risk, low AI risk

The least AI-exposed company is Ryan for the reasons covered in part 2. E&S is both complex and benefitting from carriers consolidating their points of contact. However, the E&S market is always more market cyclical than the admitted market for the reasons covered in part 3 (pricing is more volatile + risks flow in/out of the market depending on pricing levels).

WTW / MRSH / AON - Lowest cycle risk, highest AI risk

The most AI exposed company is WTW. Not only do they have a range of activities that are more prone to AI disruption that insurance brokerage, their insurance brokerage activities are also in the “susceptible” end. It’s interesting that the market also dropped WTW materially more on the OpenAI news compared to peers. Lastly, as we will explain in the next segment, WTW always seems unable to execute when it really matters. MRSH is also up there, with (for example) a management consultancy (Oliver Wyman) and benefits/pension consulting (Mercer)

At the same time, both AON/MRSH/WTW are more insulated from hard and soft-markets. Especially MRSH and WTW, who both have large non-brokerage activities. The fee-based model in large corporates is a structural buffer against soft-market price impacts (just as it causes these larger brokers to lag in organic growth in hard markets). Both MRSH and AON have slightly more cycle exposure due to both reinsurance brokerage operations (WTW lacks this) along with recent M&A forays into the middle-market.

AJG & BRO:

Both AJG & BRO benefit from the more relationship-based customers in the middle-market on AI risk. Both also have material exposures in wholesale (AJG + BRO) and AJG in reinsurance as well, which are also quite entrenched in terms of AI risk.

Brown & Brown’s recent acquisition of Accession means a material addition of E&S brokerage / wholesale brokerage activities into their previously “retail-dominated” mix. This partially makes BRO resemble RYAN from a top-down perspective (higher cycle risk, lower AI risk). As a rough guide, about 20% of AJG revenues are reinsurance and wholesale, while wholesale/specialty distribution is closer to 40% of Brown & Brown.

Gallagher and BRO also both have material cycle exposure due to their overweight in “% of premium”-based fee models and exposure to middle-market firms.

We’ve marked BRO as slightly more cycle-exposed than AJG due to the wholesale mix difference. If anything, the Q1-2026 print confirms this well… 0% organic growth for Brown & Brown and 5% for AJG.

Bottoms-up

Avoid the obvious laggard / value-trap when valuations have homogenized

It’s very common that industries have very high dispersions of return between participants based on market position, operational competence and strategies. Consider AutoZone / O’Reilly vs Advanced Auto Parts. Consider Sodexo vs. peers Aramark & Compass. CPRT vs IAA (pre-RBG). The list goes on. It’s almost NEVER wise to bet on the redheaded stepchild of the industry.

That has been WTW for quite a while. Despite continually lowered expectations from the investment community, the company has still managed to disappoint. The story is always the same for these investments “X (margins, ROIC, growth, etc.) is lower for this company than peers, if it catches up then it’s undervalued by Y%”. From an outside-view perspective, it’s extraordinarily rare that these laggards ever catch-up.

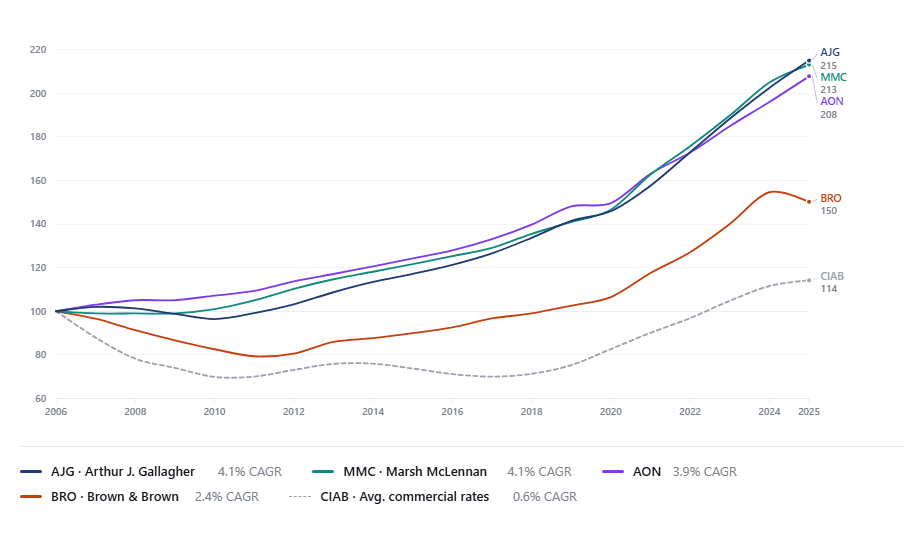

Organic growth:

If you look at the growth track record, AJG & RYAN are best-in-class. Ryan has benefitted from unique trends in E&S, so the below is only for the retail brokers:

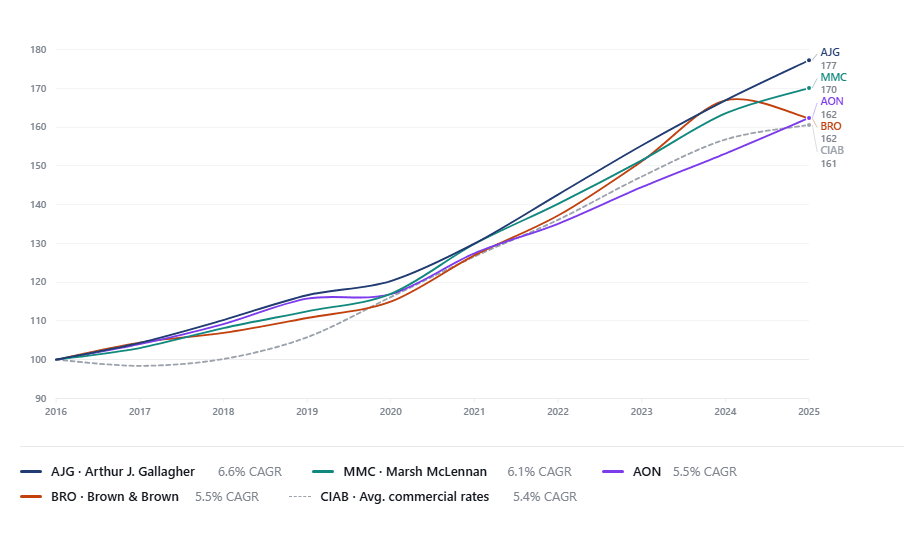

Brown & Brown is the clear stand-out loser, but more due to challenges in the 2006-2010 period, rather than subsequent performance. The same graph from 2016-2025 shows that most of the companies are in fact “roughly in-line” with each other.

In our view, the results are AJG are beyond excellent, because they have simultaneously managed to build an excellent M&A machine. This of course assumes that organic growth numbers have not been “tampered with”, which is always difficult to check in a company with many acquisitions.

Culture:

Our anecdotal experience is that Brown & Brown has a very strong culture, but that this has required several c-level executives to spin out over time and instead build their own firms. In contrast, Gallagher also has a very strong culture but has generally managed to retain high-level talent. The only thing that is slightly concerning is that CEO of AJG - Pat Gallagher - is always extremely bullish on the business prospects.

We don’t have a strong view on the cultures at MRSH, Ryan or Aon.

It’s worth mentioning that Pat Ryan (ex-Aon CEO, now Ryan chairman) has decided to give out some of his own personal shares to the Ryan employees (instead of a standard SBC plan) to further motivate people. Quite the unique signal. At the same time, Ryan is an amalgamation of recently “collected” entities, so the culture may not have “saturated” into the operational layer yet.

Capital allocation:

None of the firms are doing large enough buybacks at the current levels. All are still preferring to run M&A (their usual playbook). With that said, our view is that…

AJG is a “great” allocator of capital, especially within M&A:

Extremely long-tenured CFO Doug Howell (+20yrs)

Deep expertise in bolt-on M&A built up over +750 acquisitions, the vast majority highly succesful

Cheapest “mega-M&A” in recent years of AssuredPartners (at c. 10x operating income after synergies, c. 13x before synergies).

Recently started stepping up buybacks, but still prefer M&A. Explicitly state they are only doing the buyback due to a “woeful undervaluation” of their stock.

Both MRSH and AON recently took very big swings on mega-acquisitions. Both likely overpaid:

McGriff (MRSH, 80bn MC): 7.8bn w. seller-adjusted EBITDA of 500m —> +15x EV/EBITDA

NFP (Aon, 70bn MC): 13bn deal at +15x seller-adjusted EBITDA. Stock fell on announcement. Had to cut buybacks. Issued equity (although at high prices).

They are otherwise the standard “big corporates” in terms of cap. allocation - a dividend, some buybacks but unfortunately usually in a procyclical manner, etc.

Brown & Brown (20bn MC) did a huge 10bn deal at +14x EBITDA. Acquired both wholesale and retail businesses within Accession. Little current capital return. Looking at what RYAN’s stock has done since then (a fair proxy for Accession), they vastly overpaid for a wholesale broker at the market peak.

RYAN has continually spent big bucks (almost 20% of current market cap spent in M&A dollars in 2024 alone) at fairly “peak prices”. However unlike Brown & Brown, this was an acquisition of assets tightly within their core competence, not a foray into a new vertical. RYAN has recently started their first buyback program, due to a view of their stock being mispriced.

WTW is heavier on buybacks, but has started doing more M&A in 2025/2026. Yet they are still, by far, the buyback leader in the group, retiring 3-4% of shares at current levels p.a. - we’ve been hurt many times by buying into the value-trap laggard that had an active buyback and an attractive multiple though - so despite this (positive) SBB, the math hasn’t changed on our end.

Conclusion

WTW is out for our investments consideration given consistent lack of execution capabilities. Pass.

Brown & Brown acquired a huge asset at peak multiples outside their circle of competence. BRO is a mix of retail brokerage and RYAN, but without the integration capacities of RYAN. From what we can tell the integration is going well - but One80 (the wholesale / MGU arm acquired) was itself a mix-match of +40 companies mushed together since 2019. Adding another layer of integration onto that, while also having the remaining 60% of the business in standard retail brokerage, is a messy construct. Insurance brokers are built on optimized people & systems. If I was a BRO shareholder, I would have trouble buying into weakness, because the business foundation is still shaky from the transformative M&A. We believe there are more attractive ways to own either exposure (for example, why not just own RYAN + AJG?). Pass.

MRSH is a fundamentally good asset at good values, but it also has various conglomerate pieces that we have little interest in (management consulting especially). However the Mercer business does have several positives (for a separate article). The Guy Carpenter business is very strongly positioned in reinsurance, and the retail brokerage business is also a top-tier operation. At the right price, MRSH is interesting — but is it the most bang for your buck in a sell-off such as this? Doubtful.

AON is close to being the same story. They are trying to clean up their non-core segments by divesting part of the acquired wealth portfolio (for 2.7bn in October 2025). Marsh Re and Aon make up the two 800-pound gorillas of the reinsurance brokerage world, both have an amazing asset, however Reinsurance brokerage makes up 17% of revenue for AON and 9% for MRSH. However, the Aon wealth segment is not nearly as dominant within OCIO and other attractive niches as MRSH’s Mercer is. A good asset at a good price, but also not without some less attractive assets stapled on.

Culturally, the MRSH CEO is quite new (a few years tenure) and the Aon CEO has been on since 2005. This is not entirely positive for AON, given the amount of issues that have cropped up over time (failed WTW takeover, as one example). It’s also my understanding that Marsh is more decentralized in their thinking and approach than Aon.

RYAN is the ultimate cycle play. Whether or not one has a variant perception on soft/hard markets or admitted/E&S risk migration, it’s clear that RYAN is a truly unique asset. A big worry is that the firm has essentially been stapled together over the last few years, but given the decentralized operations this is a smaller risk than it would be in most other industries. We have an upcoming analysis to be released on whether E&S will see material reverse flow, to be released the 25th of May, 2026.

Gallagher is a core holding for us. The M&A engine is best-in-class. The AI risk is manageable. The price compensates us for cycle risk. Organic growth & execution has been consistent (and positive). The growth runway from here is either HSD in a soft market or LDD in a moderate market - at this price both are attractive. The company has not taken on “company-defining” risks to enter new verticals at peak valuations such as BRO did, so we have much higher confidence in the robustness of the existing earnings base. You get to own a premium asset at peer multiples, while those peer multiples are heavily compressed.

We will dive into both RYAN (will E&S volumes migrate back to the admitted market?) and Gallagher (why we believe AJG is the premier opportunity in the market today) in two upcoming articles.

Meritum Investments holds a position in AJG. The author may hold or trade positions in any of the names mentioned at any time. This is not investment advice.