Insurance distribution primer, pt. 1: Introduction to the ecosystem

Part 1 of our primer on the insurance brokerage industry

We have been following insurance brokers for more than half a decade. They are among the most reliable wealth-compounding businesses in modern public markets: asset-light, high-retention, with consolidation opportunities through M&A. They have been bombed out twice during the last years: briefly during the 2020 pandemic crash, and again today. These brokers are never unprofitable, rarely grow earnings below 6% per year, and generally spit out excess cash year after after.

This is the first of a four-part series.

Part 1 (this piece): What insurance brokers actually do, why the ecosystem is so layered, who the main players are, and why valuations have compressed.

Part 2: AI risk. Why retail and wholesale face fundamentally different AI questions.

Part 3: Cycle risk. What a soft market actually does to broker earnings.

Part 4: Picking your horse: A framework for choosing between RYAN, AJG, BRO, MMC, and AON given today’s prices

A lot of money has been made owning high-quality insurance brokers for the last decades, and we don’t believe that will change moving forward. But the industry can be difficult to understand. In fact to most, the whole idea of insurance brokerage sounds weird. Let’s give an example:

Insuro-world

You operate Newsletter LLC and want to open a bank account. In the real world, you walk into a bank, fill out a form, and receive a debit card the next week.

In Insuro-world, none of this happens.

You contact a retail banking broker, who handles your basic deposit account and credit cards.

For your bespoke working-capital facility — funding coffee and sweets between article payments — your retail broker is too generalist, so they reach out to a wholesale banking broker who has placed working-capital facilities for newsletters every week for the last fourteen years. The wholesale broker negotiates with the bank.

Except the bank doesn’t actually have the in-house expertise to evaluate newsletter working-capital risk, so it has delegated the design of the credit program to a third-party specialist who sets the terms and signs paperwork on the bank’s behalf — while the loan still sits on the bank’s balance sheet. The bank, in turn, has reinsured the risk to a syndicate of capital providers it has never met. Your bank, as it turns out, has retained essentially none of the actual exposure.

Working with the bank in this world is like going through a nasty divorce. Only the middlemen are talking to each other.

This caricature is unkind to commercial insurance, which has perfectly good reasons for looking the way it does. But the structural absurdity is exactly right: an industry where the customer rarely meets the risk-bearer, and where the chain of intermediaries between them captures something like 25-35% of the underlying premium dollar.

So how does it actually look in insurance?

Insurance distribution / insurance value chains are complex. There are essentially two markets. In the admitted market, the form & price of the insurance contracts are regulated. This helps standardize risks & require less expertise to manage. These are the standard commercial retail brokers. They help a business get coverage for property damage, auto damage and workers compensation.

Admitted market:

Business —> Retail broker (represents business) —> Carrier (insures business)

Sometimes, the carrier can use agents to represent themselves.

E&S market:

However some markets handle complex risks, either recently emerged (insuring large data-center construction projects) or risks that require more specialized contracts (cybersecurity for a Fortune 500 customer). These contracts belong in the Excess & Surplus market (E&S). In this market, there is freedom of form and price, as long as the carrier can prove the risk is not priceable in the admitted market.

Here, the chain can involve multiple parties.

Business —> Retail broker —> Wholesale broker (Advisor for Business)

Carrier —> Managing General Agent/Underwriter (Runs program for carrier).

The MGA is an expert in a certain sub-niche, for example construction risk for offshore wind farms. This risk is not placeable in the admitted market, but the carrier does not have expertise or volume to built a full internal organization for pricing offshore wind construction risk. Instead the MGA is akin to a hedge fund, pricing risk on behalf of its LPs (carriers) and receiving fixed (volume-based) fees and performance fees.

Reinsurance:

Finally, some carriers don’t want to own the full risk they have. They sell off either a fixed share (quota) or just the left tail (excess-of-loss) of their policy risks to reinsurers. Here they also employ reinsurance market specialists, which are dominatead by Gallagher Re, Aon, Howden Re and Guy Carpenter (Marsh) in a strongly concentrated oligopoly.

Carrier —> Reinsurance broker —> Reinsurer

Fronting carriers:

Lastly, there exists a rare construction (but growingly relevant) where the carrier is just a “piece of regulatory paper” - essentially a fund-of-funds for reinsurers. The carrier has no other activity but to facilitate reinsurer capital writing policies. The “Fronting” carrier employs MGAs to write the risks, and immediately passes the risks to reinsurers. Essentially the MGA (experts in underwriting) and reinsurers “team up” through a fronting carrier:

Wholesale broker ← MGA ← Fronting carrier (no risk taken) ← Reinsurer (real risk taking)

Why insurance is so layered

Banking is not like this. The structural reasons commercial insurance is:

(1) Insurance is adversarial. Banking products generally have win-win economics — both sides want the loan repaid, the credit card to function, the deposit to clear. Insurance is closer to a structured bet: you are paying for a contingent payout where your counterparty has 1,000x more pricing experience than you do. You want a professional on your side. The retail broker is your professional. The wholesale broker is the retail broker’s professional.

(2) Policies are infrequently used and disproportionately important when used. You can intuit whether 7% or 15% is a fair interest rate. You cannot intuit whether your commercial auto policy adequately covers your exposure to a multi-truck pileup with a fatality and a sympathetic plaintiff in Cook County. Most insurance buyers correctly conclude they should outsource answering that question.

(3) Insurance is regulatory plumbing as much as risk transfer. Compliance with state-, federal-, and contract-level requirements is not optional. A specialist knows what is mandatory, what is typical, and what is negotiable. You don’t.

(4) Risks are heterogeneous in a way banking products are not. Each business has unique exposures, and the carrier base wants diversification across many specialized niches without having to build dedicated underwriting expertise in each. The MGA model exists precisely to bridge this gap: insurers want exposure to specialty risks, but cannot economically build internal teams to underwrite them. They delegate to MGAs.

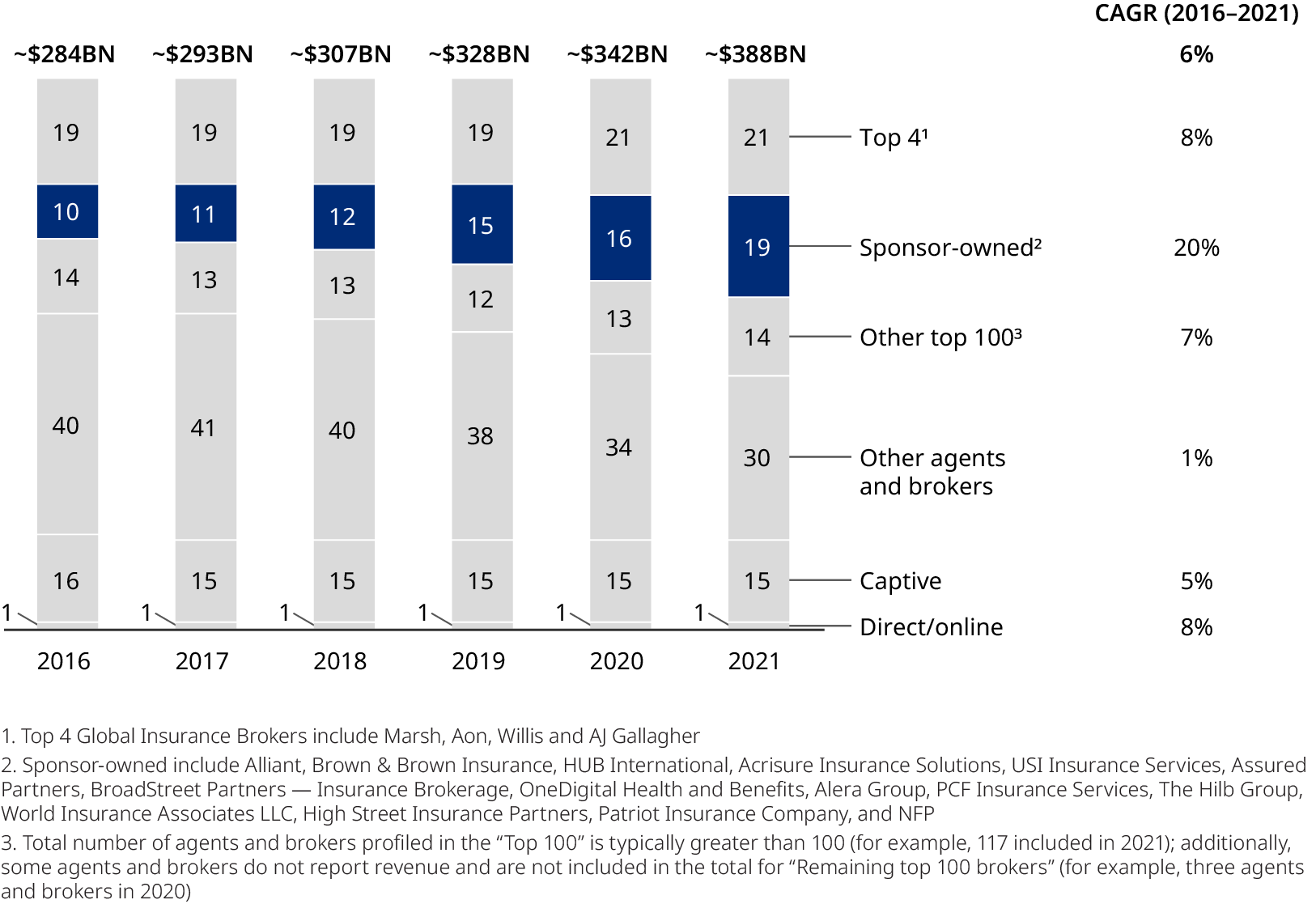

The result of (1)-(4) is a market where the customer wants an expert, the carrier wants distribution scale, and the gap between them is wide enough to support multiple specialized intermediaries. In the UK, +90% of commercial insurance is brokered. In the US, per Oliver Wyman: roughly 84% brokered, 15% captive (self-insured), 1% truly direct.

The market has effectively concluded that only fools negotiate their own commercial insurance, at roughly the same rate that defendants represent themselves in felony criminal proceedings. This is a structure with very deep roots. It does not change quickly.

Who’s who:

The big ones:

MRSH (Marsh McLennan) is a bit of a conglomerate. It owns Oliver Wyman (Management consulting, created the chart above) and Mercer (Benefits & compensation specialists), but the majority of earnings are driven by Marsh (Retail brokerage) and Guy Carpenter (Reinsurance brokerage). MRSH is really strong in large accounts, but has focused it’s M&A muscle on growing into the fragmented retail mid-market.

AON (Aon) is the second “large” peer. Has a very strong presence in the top-tier clients of insurance brokerage, and has a very strong reinsurance presence. Has also used its M&A muscle recently to move further down into the mid-market.

AJG (Arthur J. Gallagher) is our favorite broker. Dominant middle-market specialist with a prolific M&A engine (+750 deals), strong reinsurance presence, strong wholesale presence, strong retail presence and a few other bits & bops added on as well (claims management, benefits). Best-in-class organic growth.

BRO (Brown & Brown). Great ticker. Middle-market and small company specialist. Also prolific on M&A, but slightly lumpier and weirder deals. More volatile on organic growth. Similar to AJG in having family-members as CEO. Recently completed a very large, transformative, deal that also moved them into wholesale brokerage and being an MGA.

WTW (Willis Tower Watson) the red-headed stepchild. Long dismissed as a failed integration where nothing could “go right”, they have started stepping up their organic ambitions, have a strong benefits/compensation/pension advisory franchise and trying their best to improve broking business. Used to own the Gallagher reinsurance operation before having to divest for anti-competition reasons.

E&S specialists:

RYAN (Ryan Specialty) is a wholesale expert broker, focusing on MGA + wholesale brokerage (with a side of binding authority, which is just “MGA-light”). Created by the former Aon CEO, Pat Ryan. Has been absolutely amazing the last few years on organic growth, but has a much greater cycle sensitivity than the broader retail brokers.

AmWINS and CRC Group are both private. But these are two main competitors in the E&S market.

Carriers:

Standard (admitted) carriers, you know most: Travelers, The Hartford, Chubb, Liberty mutual, etc.

E&S / specialty risk: Markel & Berkshire as two famous ones

Fronting carriers: State National (built by the Ledbetter family and sold to Markel, above). Accelerant (ARX). Trisura, Kestrel Group (public, same Ledbetters who built State national).

Why do you want to own brokers?

Asset light: Brokers can grow without reinvesting profits into tangible assets.

Low risk operations: They carry no policy risk. None of the insurer’s loss volatility shows up on a broker’s P&L.

Predictable revenues: Customer retention runs +90%, even +95%. Cyclicality affects how much each customer spends, but customers are very sticky. This makes brokers robust, predictable business models with limited absolute downside in the short term. Insurance policies are renewed annually and each time, the broker gets a piece of the action.

Highly profitable: Operating margins run 25-30%+. Returns on tangible capital are very high.

M&A optionality: They can roll up smaller agencies at 7-10x EBITDA.

Brokers are, in other words, an asset-light, high-retention royalty on commercial insurance premium growth, with optional consolidation leverage from M&A.

Insurance brokers will earn a profit each year. It is simply a question of how fast they will grow, and whether the growth algorithm justifies the multiple.

Great business, but so what?

Well, first off - the market has soured on the insurance brokers in general:

Stuff goes down for many reasons, and not all of them are buying opportunities. The most common bear trap is buying an industry that has merely re-rated from “extremely high multiples” to “high multiples.”

Starting multiples were elevated but not extreme — most names traded at 20-25x forward earnings during 2023-2024. Today the major retail brokers all sit in a tight 15-17x NTM P/E band. EV/EBITDA tells the same story:

(The Ryan EV/EBITDA is off - Ryan has c. 1bn of EBITDAC, 3bn of net debt ex. fiduciary cash and 10bn market CAP - i.e. 13x EV/EBITDA(C) … in line)

Yet the industry has not yet seen any material reduction in profitability, nor are analysts expecting any big trouble looming in the next 12 months, as shown by the normalized consensus average EPS expected by analysts, for any forward twelve month period in the last 5 years:

The above graph demonstrates the consistent growth pattern that has historically benefitted insurance brokers tremendously. Consistent, non-volatile earnings (expectations) increasing over time. Yet it also shows that the stocks are not down due to any realized negative events. It’s currently entirely due to narrative fears. Only the more cyclical Ryan has seen a slight downward revision.

The forward-twelve-month consensus EPS for every major broker is essentially flat to up over the last twelve months. The stocks are not down because of realized fundamental damage. They are down on narrative.

The narrative is two-headed:

AI will disintermediate commercial broking. The strongest version of this argument: large language models can read policies, compare quotes, and handle claims correspondence. Customers go direct. Commission rates collapse. There are various “weak form” versions that also spell trouble for brokers.

A soft market is incoming. The reinsurance market has softened materially after three good years. Property is rolling over. Commercial rate increases which had been running +5-15% across most lines through 2022-2024 are compressing toward flat in 2026. This hits the commission rate 1-to-1 for brokers, but is partially compensated by increased volumes.

Which narrative you favor (if any) has a heavy impact on which of the companies you expect to outperform, and which ones will face growth headwinds.

We will cover the AI narrative in Part 2, the cycle narrative in Part 3, and our takes on “which name to own” in part 4.